With great versatility comes great responsibility – don’t give up on absolute return for retirement.

When it comes to retirement, the needs of Britain’s savers are defined by factors such as goals, wealth, and personal circumstances. However, for the most part, these investors require financial solutions that can support their income, grow in line with inflation, and leave a pot of money for their family to inherit.

Since the introduction of pension freedoms back in 2015, targeted absolute return funds have become an increasingly popular option for those entering the decumulation phase of their financial lives. Given what the funds were established to offer, this is not surprising with low interest rates and against a low-return backdrop in annuities and other traditional retirement solutions.

Indeed, Dynamic Planner has just announced the launch of its Risk Managed Decumulation service comprising eleven funds such as Church House Tenax Absolute Return Strategies, the ket attraction being the low volatility of returns which permits regular withdrawals of capital & income with little risk of reducing the value of capital invested.

In its purest form, the absolute return approach suits the needs of many retirees perfectly. It should provide consistent, smooth returns that can be top-sliced without diminishing principal investment against any backdrop. However, the reality is quite different. In recent years, the sector has come under much pressure as many constituents have fallen short of their goals.

As defined by the Investment Association, absolute return funds are managed principally to deliver positive returns in any market condition- often expressed in terms such as “cash plus”. The products are not benchmarked against a specific sector or index and must clearly state the period over which they intend to deliver their target return – a rolling timeframe that cannot exceed three years.

Problems are likely to arise in any sector whose definitions contain vagaries, let alone a sector who’s underlying funds invest across many different assets and geographies. Capital preservation, rather than ‘cash plus,’ should be at the heart of any absolute return fund.

It’s no secret that after years of quantitative easing, many investors have been drawn higher and higher up the risk scale in search of income and/or growth, therefore potentially subjecting investors to major and unexpected losses. The pursuit of growth while disregarding capital preservation seems like a reckless strategy.

Some assets look uniquely vulnerable in certain environments and investors have to ensure that their absolute return fund is going to protect them in all market conditions, not just the benign ones. They should not be seduced by low volatility into thinking that capital preservation is easy.

Given the shrinking pool of income-generating options in “traditional” asset classes, the enhanced versatility offered by absolute return funds, when applied with caution, is key to providing the sort of consistent, low volatility returns required for decumulation.

In recent years, many absolute return products at the more aggressive end of the sector have begun to take on increasing levels of risk to achieve their objectives against a backdrop of broadly rising markets. This has led some to shoot the lights out in one year before crashing just as heavily in another when markets change.

For retirees wanting to draw income from their portfolio, such volatility can become a real issue due to something known as “sequencing risk” – also known more colloquially as “pound cost ravaging”. These terms describe the process by which taking income from portfolios in falling markets can leave capital depleted and, in turn, income permanently lower.

After all, while a 10% loss in any one year would require an 11% gain to break even, a 30% loss requires a rise of 43% to break even. Relatively short-term losses can have a lasting impact, and drawdowns only emphasise this.

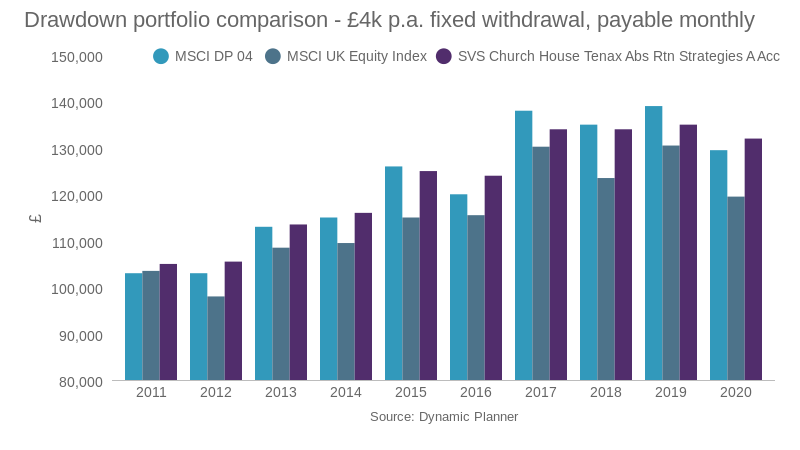

The graph, right, from Dynamic Planner shows the difference in portfolio value over time for the risk benchmarks, DP8 and DP4, as well as the Church House Tenax Absolute Return Strategies Fund, itself rated DP4 as a decumulation vehicle. The chart assumes a 4% annual drawdown scenario. The difference is immediately apparent, and it’s clear that a lower volatility of returns is preferable for a drawdown vehicle.

Broadly speaking, then, an absolute return fund that delivers volatile returns risks undermining the purpose of absolute return investing. It is therefore imperative that investors do the research needed to identify the products in the sector most likely to provide smooth returns.

These are the products that start from a base of capital preservation rather than ‘cash plus’. And those which have historically delivered a smooth path of growth and consistent income across market cycles rather than a volatile growth curve inappropriate for retirees looking for consistency in returns. There are several ways that this can be done:

By checking time frame: The shorter the period the manager has given themselves to meet their goal, the less scope they have for volatile returns and the less likely they are to take on excessive risk.

By checking performance: In cases where funds have been running for long enough, check every possible rolling period to see if it met its goals. Likewise, check performance over annual periods. If outperformance is remarkable in one-year, then consider this a red flag – the same degree of underperformance could follow in another 12 months.

By checking maximum drawdown over a certain period: This is an excellent way of assessing the amount that would have been lost if an investor had sold at the worst time. The lower figure, the better.

Absolute return funds adhering to the core, original principles of the concept are actually an ideal option for retirees looking for a consistent annual income while minimising the risk that they will deplete capital over time.

In the recent market sell-off, the reputation of absolute return funds has been restored somewhat following a few difficult years during which a number of the larger funds produced disappointing results. However, investors in the sector should be looking carefully at a manager’s definition of absolute return; what they are trying to achieve, as well as historic performance, drawdown, volatility and the type of risks they are taking.

For the record, the Church House definition of the absolute return objective is the delivery of positive returns in excess of cash plus fees over rolling twelve-month periods. We view an objective of cash plus 3% or plus 5% over longer periods as ‘targeted return’ for which a higher level of risk is required than for absolute return.

First seen on Retirement Planner online.

How would you like to share this?