The FTSE 100 continued its fall from the end of February and resulted in a peak-to-trough fall of 35% for the index year to date.

Coronavirus has led the global population into lockdown, hitting the travel, leisure and retail sectors hardest. Additionally, an oil price war between the Saudi’s and Russians added to the perfect firestorm.

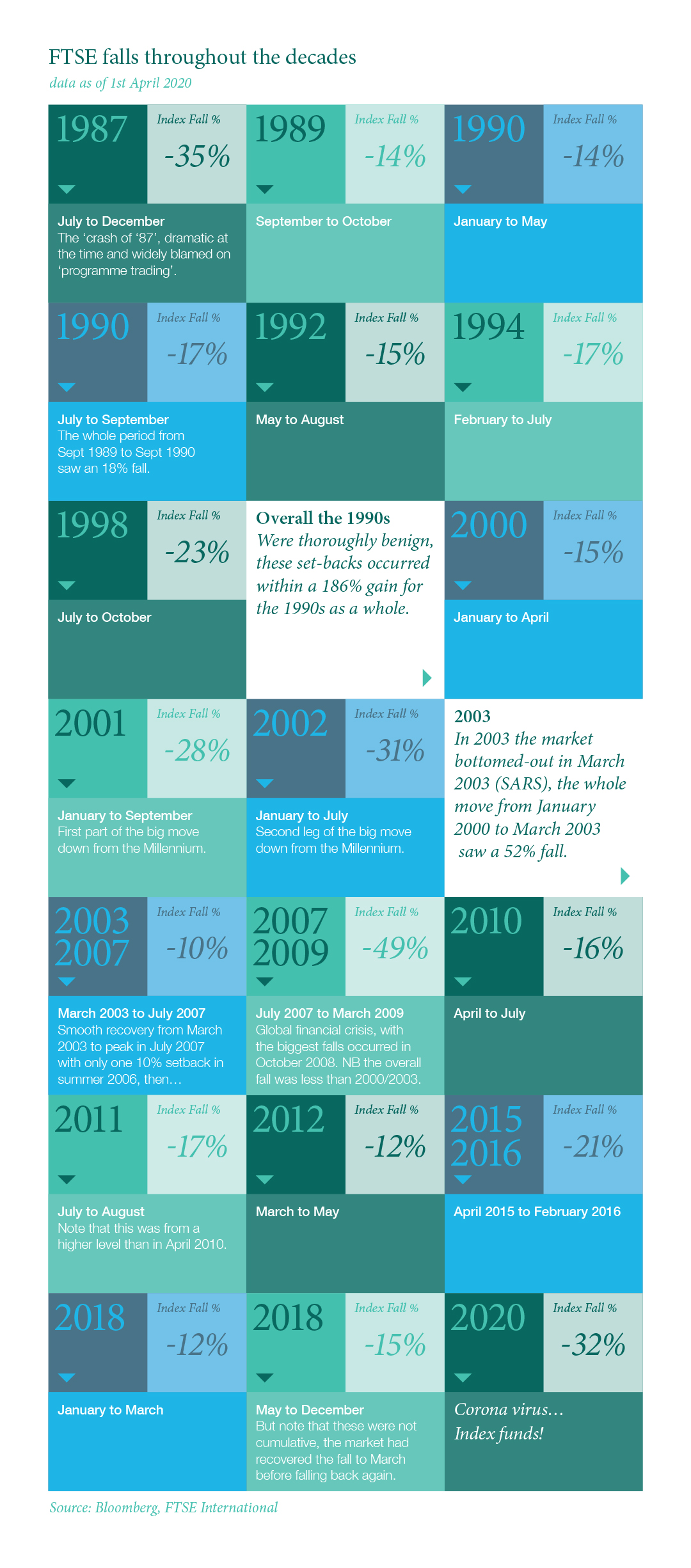

In the midst of the stock market crash, it is easy to forget that the price of Brent fell to $22 a barrel at the same time. Who knows how the Index funds and trackers affected the sell-off, but according to one of our brokers, over 50% of the volume on the darkest day, during the height of the meltdown, was from the ETFs and Index trackers solely unwinding their positions in a free-falling market attempting to keep to weight...

Fortunately, we went into the period with a cash position and, in the spirit of Warren Buffett, we attempted to be greedy when others were fearful and used the opportunity presented to deploy the dry powder and initiate new positions and add to existing holdings that we believe had been unfairly and unduly hit.

Amongst those topped up (far too many to list them all) were the highest quality companies we refer to as our ‘FTSE All-Stars’, including Halma, Diageo, Diploma, RELX, Spirax-Sarco, Experian and Fever-Tree. In the, smaller, international element of our portfolio, which performed strongly against their more domestic peers, we added to Microsoft, Investor AB and Heineken.

As the market appeared to find the bottom, it threw up many companies with extremely attractive stock valuations. We initiated positions in companies that we have long-admired and modelled, but previously had been too fully valued to justify investing in.

Trainline and Auto Trader are exactly the sorts of high quality businesses we like; platform businesses, capital and asset light, highly cash generative and the clear market leaders in their sectors.

For Auto Trader, clearly in lockdown no one is buying cars but their balance sheet is strong and management excellent, outlined by their decision in a 5% placing for the company when the market was awry and any share price momentum wouldn’t be affected.

Trainline, equally lacking in near-term revenues due to the lockdown, a 60% fall in the share price was a very attractive entry point, especially for a business we like.

Additionally, we reinitiated a position in Berkeley Group, the house builder, who was also hit hard. It has an exceptionally strong balance sheet and pipeline - a net cash position of £1 billion and a consented land bank of £750 million.

They are the highest quality business in their sector and, with a strong management team were trading just shy of £60 a share a fortnight before we picked them up at almost half that.

Our focus on the bottom-up fundamentals of companies is allowing us to identify a number of attractively priced, high-quality investments which we believe will stand the CH Equity Growth Fund in good stead in the eventual recovery in stock prices.

How would you like to share this?