From mid-September risk assets took a further turn for the worse with an extraordinary display from the new UK Government leading to UK assets being in the vanguard.

The US Federal Reserve and the European Central Bank (ECB) raised their base rates by 75bp, the Bank of England limited itself to 50bp (in a split decision), though, to be fair to the Bank, it was the day before the UK Chancellor’s ‘fiscal package’ announcement. The Fed is continuing to signal that more tightening will be needed to bring inflation back to target while admitting that an economic contraction is a means to this end. Risk assets continued the sell-off that began in mid-August and bond yields rose.

Then came that hopelessly ill thought-through fiscal package. How on earth the new Government could think that announcing a raft of tax cuts, with no indication as to how these might be financed, might go down well with the Gilt market is a mystery. At a time of high inflation, adding the necessity for huge extra borrowing onto a market already uncertain and expecting the Bank to be selling its own Gilt holdings (that quantitative tightening that was due) was a misjudgement (to put it mildly). The Gilt market duly collapsed with some quite shocking moves, most notably amongst long-dated index-linked stocks (the longest of these, launched in November last year, has subsequently fallen an almost unbelievable 86%!).

As has been widely reported, the Bank had to step in to calm the Gilt market and restore some order, which has been successful. But the interesting part of this is the complete re-pricing of the UK yield curve back to levels not seen since 2009, the long Gilt yield being firmly back in the range that persisted from 1998 to 2010.

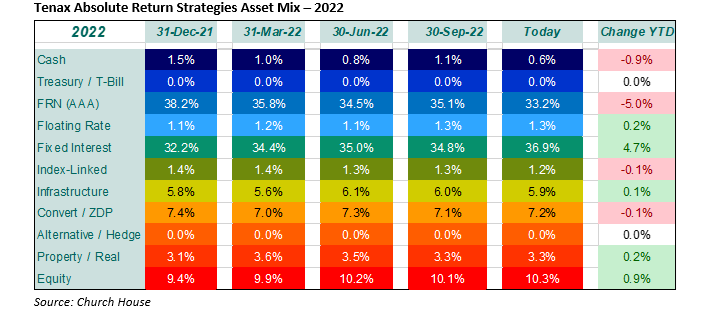

The period has been particularly uncomfortable for Tenax. The steep falls in the Gilt market, particularly over the final two weeks of September, took their toll right across asset classes. The weighting in floating rate notes (FRNs) was the anchor for the portfolio, otherwise there was essentially nowhere to hide. Within the Fund, we continue to edge our FRN exposure lower to take advantage of the opportunities that are being presented in (short-dated) credit markets, as shown on the right.

Looking down the asset classes, the Floating Rate Note exposure is now at one third of the portfolio. Yields here (now at 2.75%) are moving up with the Base Rate and will follow any further increase next month. We expect the Bank to add a further 75bp in November, so our FRN yield will then head for 3.5%.

Credit spreads have widened again, unsurprising in the circumstances, so we are adding to our Fixed Interest exposure gradually, while not increasing the short duration. It is worth stressing the height that these (short-dated) redemption yields have reached and what this means for the portfolio:

The redemption yield on this portion of the Fund (37%) is now 7.25% with a duration of 3.8 (the overall duration including the FRN book is just 2.1). The average price of the issues that make up the Fixed Interest proportion of the portfolio is 82p so, sitting on our hands, we have that ‘pull to par’ – maturity at 100p – to come, in addition to the income stream.

We have not made many changes in the other asset classes, considering that the opportunity in short-dated credit was the key consideration. Infrastructure has been hard hit by the move away from long duration assets and we have not made any more changes, considering that the investments we have are in a position to weather the storm. The Convertible holdings are unchanged while exposure to Zero Dividend Preference is reduced again following the maturity of a NB Private Equity issue. We have added slightly to Equity where opportunities are also emerging, notably amongst UK stocks.

We fully expect the central banks to raise their rates further (well, certainly the Federal Reserve and Bank of England) and it seems likely that we might face more bouts of extreme volatility. Inflation remains the key to any genuine change of mood, though this is an indicator that lags, and it might be more correct to say that markets are unlikely to recover in a meaningful way until it can feel that the Fed really means what it says and that a turn in inflation appears likely. But we do think that it is time to take a step back from the frenetic atmosphere and consider carefully the smorgasbord that is now on offer out there…

The above article has been prepared for investment professionals. Any other readers should note this content does not constitute advice or a solicitation to buy, sell, or hold any investment. We strongly recommend speaking to an investment adviser before taking any action based on the information contained in this article.

Please also note the value of investments and the income you get from them may fall as well as rise, and there is no certainty that you will get back the amount of your original investment. You should also be aware that past performance may not be a reliable guide to future performance.

How would you like to share this?