Following the trend from last month, the emphasis in transactions has once again been in the credit markets.

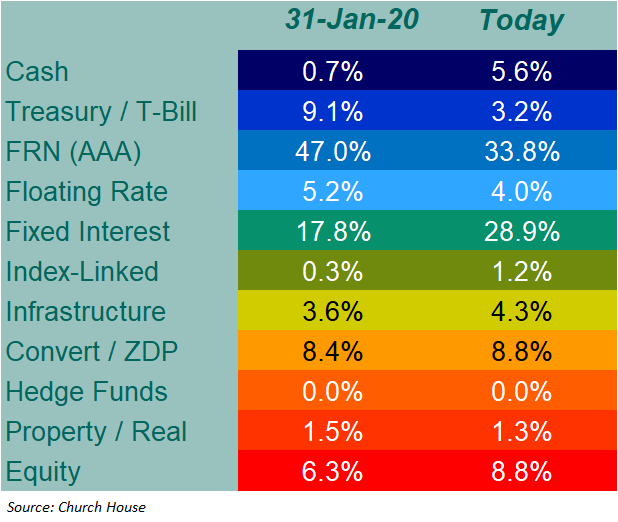

The change illustrated in the table, see right, since pre-crisis levels at the end of January is now clear to see.

Credit investments now account for more than 30% of the Fund’s portfolio. Equity, convertible and infrastructure have also increased, particularly when taking account of the falls in these areas over the period. Against this, the triple-A floating rate note portion is markedly lower. It is not that we dislike FRNs now, they continue to provide useful returns, but it is simply that the opportunities are now elsewhere.

The primary market in credit has been extremely busy as companies, encouraged by the backstop of central bank liquidity, came to the market to raise funds. We have participated in a number of these, including new issues from Southern Water Services, GlaxoSmithkline, Legal & General and bank issues from Barclays, Citibank (USD issue) and Lloyds. We also added to several existing holdings as we saw opportunities and, rarely for Tenax, an index-linked issue from Heathrow Funding.

Though the volume of transactions has been in the fixed interest markets, we have not ignored equities, which have stabilised further over the month. We added further to the holding in Smith & Nephew but took the profit on the holding in William Morrison, which had been more of a defensive position. We acquired a new holding in Compass Group, both in the market and in their placing, while adding further international equity exposure and some private equity.

How would you like to share this?