My view is that some expensive markets, practically all sovereign debt, have become even more expensive, while other expensive markets e.g. US equities, credit markets (quality only), have flipped to looking cheap again.

However, I have few pearls of wisdom to offer regarding short-term moves in the markets. In the current febrile climate (the BBC appears to think that we have bubonic plague stalking the country) there is no telling where the emotion might take us, and Americans know how to ‘do’ emotion.

The global impact of COVID-19 continues to unfold

I am certainly not qualified to give any medical advice on COVID-19, simply to observe that the spread of viruses appear to conform to a statistical pattern. Around the world, countries are competing to set harsh restrictions on gatherings and travel while central banks and governments are ramping-up their economic support mechanisms. Sadly, President Trump appears to be a shade ‘behind the curve’.

JPMorgan is maintaining some excellent statistical analysis on the spread of COVID-19, to quote their report published on 17th March: “China continues to recover strongly… active cases are now below 10,000, which to us implies that by the end of this week a large proportion of COVID-19 cases in China will have recovered.”

With regards to Italy, they observe that the rate of change of new cases continues to slow with a peak in sight. The rest of Europe can expect increasing cases numbers for a few weeks yet, the UK appears to be on the optimistic side of the curve but can certainly expect to see cases increasing for a while yet.

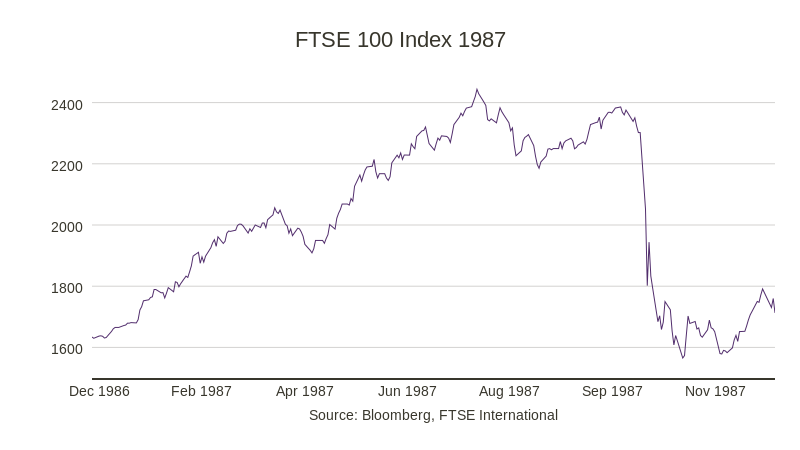

Stock prices appear to be competing to outdo October 1987 in the severity of the short-term falls. Between early October 1987 and early November, UK stocks fell 34% (October 19th being the worst of it). This time we have fallen 32% from 20th February to date.

Then, ‘programme trading’ was blamed for much of the leap in volatility and loss of liquidity, this time I suspect that ETFs are probably doing a similar job. But, of course, each bear market is different.

The virus provided the trigger for this one, how long it persists and the economic damage it does en route will determine its length.

Measures we are taking

Meanwhile, we are all fit and well at Church House. We have split the fund managers down into small groups in different places, as we have with our settlement and compliance staff and have robust disaster recovery procedures in place if required.

We are all quite used to working remotely and are not experiencing any technical problems. All company and broker meetings are being carried out by conference call.

Church House itself has a robust balance sheet, we maintain substantial cash, and we have no debt so remain strongly placed to continue to service the needs of our clients and investors.

How would you like to share this?