After a grim year and the slightly better tone to markets in late-October and November, December returned to worrying about central bank action and was generally a negative month.

The final quarter of the year does still show positive returns and it may be that late September will mark the lows, though big tech will need to show some signs of life soon to feel at all confident about that as far as the equity markets are concerned.

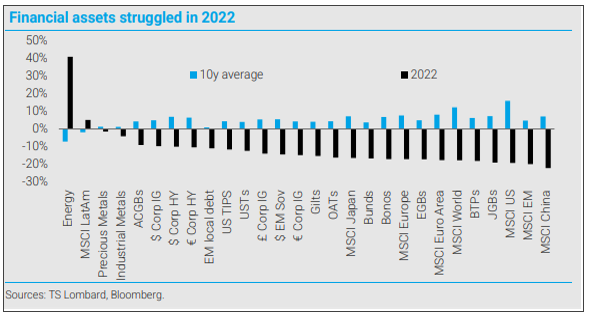

TS Lombard’s table of international returns for 2022, compared to their ten-year averages, sums up the year (right).

The Federal Reserve, ECB and Bank of England all raised their base interest rates by 50bp in December, earlier expectations had been for more 75bp increases. But another pleasant surprise from the US inflation figures for November, marking the fifth monthly decrease, tempered the Fed’s response. The Bank of England’s 50bp increase was accompanied by the rather discouraging note that two members of the Monetary Policy Committee had voted to leave rates unchanged at 3% and one had voted for an increase to 3.75% (it is a nine-person committee). But markets were rattled again by the accompanying ‘tough talk’ from central bankers, the hardest to swallow was the commentary from the European Central Bank:

“We decided to raise interest rates today, and expect to raise them significantly further, because inflation remains far too high and is projected to stay above our target for too long”.

That’s rich coming from the Bank that waited so long to take any action at all, despite what was happening and multiple warnings from observers. Inflation began to move away from the ECB’s target zone in summer 2021, but it was not until more than a year later, in July 2022 that they even managed to lift their rate off the floor, all the while carrying on with quantitative easing (pumping ever more money into the system - no wonder it fell in value...)

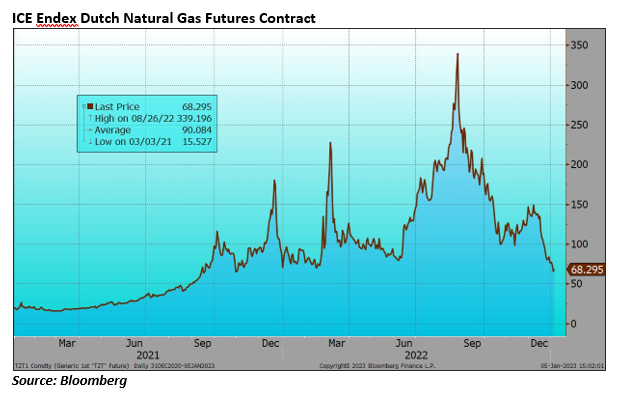

It would appear that we have seen the peak in inflation rates, with figures from France and Germany over the past few days encouraging this view. Some improvement in UK figures would be welcome. European gas prices also provide some encouragement having fallen further in recent weeks (see below), while European gas reserves are now higher than at this time last year before Putin’s war, that is an achievement.

ICE Endex Dutch Natural Gas Futures Contract (right)

US ten-year rates moved back up to close the year at 3.9% (they started the year at 1.5%), the UK ten-year to 3.6% and a leap for the German ten-year to 2.6% after those comments from the ECB (that German ten-year was on a negative yield in December 2021). So, bond markets suffered across the board. Equity markets also sold-off again, led by weakness in the NASDAQ and big tech. Few avoided the sell-off, Alphabet, Amazon and Apple all fell by more than 12% over the month while Tesla was damaging sentiment with a 37% fall. The financials provided a few bright spots, notably the Japanese banks which leapt on the first signs of an easing of Japan’s clamp on rates.

Looking at prospects for 2023 the principal concerns that we can identify at this stage must be:

- Have we seen the worst of inflation?

- How far will the Federal Reserve (and the other CBs) go?

- Will the recession be worse than currently expected?

- Is there an endgame in Ukraine or does it get worse?

As above, it appears likely that we have seen the worst of the inflation for now, encouraged by the recent US figures, early indications from France and Germany and the continuing fall back in energy prices. The Federal Reserve appears to have restored its credibility (but at a cost); the ECB just looks foolish. The concern must be that the central banks go too far and make the recession worse than necessary. For the moment it appears that the recession should be relatively mild, but this could change. The war in Ukraine has all the hallmarks of a long drawn-out and unpleasant conflict, we can only hope that the Ukrainians can maintain their determination, and the West continues to help.

Overall, we consider that there are attractive opportunities to be found in a number of the asset classes after last year’s ‘re-pricing’. Shorter-dated corporate fixed interest (credit) is definitely interesting now with credit spreads still wide. With yield curves inverted (higher short-term rates than long-term) in many centres, the attractions of longer-dated fixed interest diminish quite quickly and do not reflect the residual risk. Equities are more difficult as earnings will fall with recession, but they have been ‘re-priced’ in dramatic fashion. Last year’s switch from quality to recovery/value was largely nonsense and here there are plenty of opportunities. Overall, we expect stock markets to ‘climb a wall of worry’ but it is unlikely to be plain sailing.

From a geo-political perspective, it is also encouraging to note that the two major world dictators, Vladimir Putin and Xi Jinping, are looking somewhat hobbled. To quote Holger Schmieding (Chief Economist at Berenberg):

“Having started a brutal war, Putin has no easy way out. Ukraine and the free world are standing up to him. The expenses of war, the slow poison of sanctions, the flight of parts of the urban elite and the mounting costs of repression will be a worsening drag on Russia as long as Putin remains in power. In China, the red emperor has lost some of his clothes, having failed badly to prepare his country to live with the COVID-19 virus. Excessive government intervention, mounting domestic debt and – most importantly – the risk of further grave policy errors by a leader who believes his own propaganda suggest that China will be far less vibrant in the future than in the last three decades. For China under Xi, overtaking the US may remain a pipedream rather than a realistic prospect.”

Happy New Year

The above article has been prepared for investment professionals. Any other readers should note this content does not constitute advice or a solicitation to buy, sell, or hold any investment. We strongly recommend speaking to an investment adviser before taking any action based on the information contained in this article.

Please also note the value of investments and the income you get from them may fall as well as rise, and there is no certainty that you will get back the amount of your original investment. You should also be aware that past performance may not be a reliable guide to future performance.

How would you like to share this?