Last month in this commentary, I was writing that February had seen a sharp reversal that took US ten-year yields back over 4% as central bankers fretted over stronger economic data.

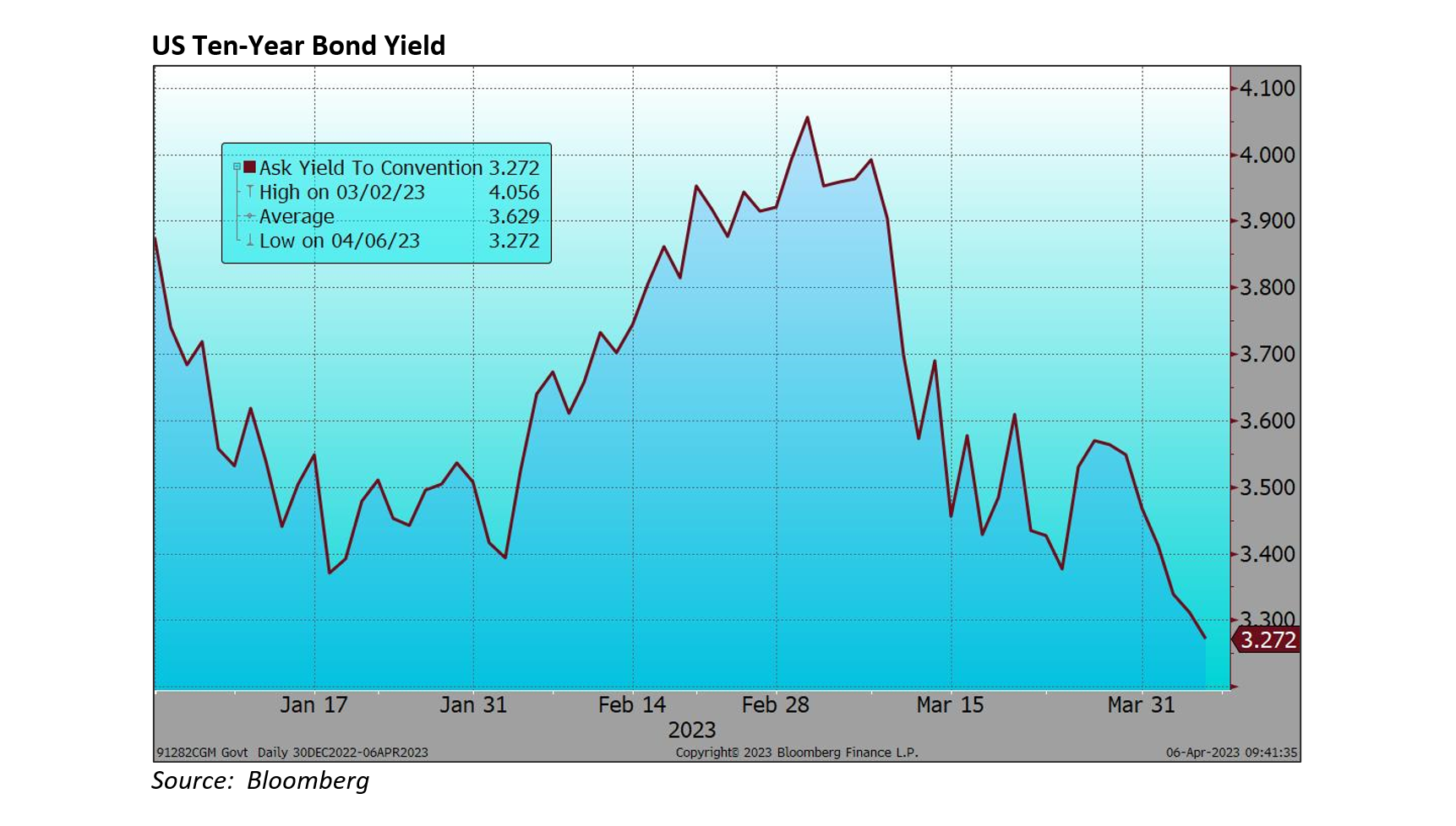

A month being a long time in these markets, February’s sharp reversal has reversed (right).

That move takes US yields to a six-month low, the same being true for two-year yields. Of course, in the meantime, the Bank of England, ECB and Federal Reserve have all raised their base rates, though with much stress on ‘data dependency’. Clearly, market rates are saying that it is time to move on and not indulge in too much handwringing over ‘core inflation’.

Which takes us to other lagging indicators and the small matter of another banking scare. Late last year, Jerome Powell, Chairman of the US Federal Reserve, said that he wanted to “bring some pain”, and has since raised rates another three times. Tightening credit conditions like this does take time to work through individual and corporate decision making and this has been a v rapid sequence of rate increases. The sudden demise of Silicon Valley Bank demonstrating that while the effects of central bank tightening can take time to work through the system, a bank run can happen in the twinkling of a social media post.

The resulting scare rattled around the bank sector and quickly claimed another scalp with the collapse of Credit Suisse (into the welcoming arms of UBS Group). Perhaps this was not a surprise as Credit Suisse has been lurching from crisis to crisis over the past few years (Archegos Capital Management etc etc). The collapse of practically all bank share prices was excessive and this is gradually correcting. It has certainly shaken up the regulators and the sheer pace of events has, in itself, provided a further shock to the system and, undoubtedly, acts to tighten credit conditions further.

I do hope that the central banks will recognise that it is time for a pause, credit conditions are significantly tighter now and demand for credit is waning fast. It appears that Jerome Powell recognises this, I hope the realisation can spread to the others. The immediate ‘banking crisis’ appears to have been contained quite quickly but, doubtless, there will be more of a witch-hunt yet.

Stocks have been caught between an incipient banking crisis (and falling bank stocks) and the prospect that ‘peak rates’ might be here. American stocks have made small gains while the UK and Japan have fallen back, the NASDAQ is still the lead market for the year to date led by the tech heavyweights (Apple, Alphabet, Microsoft) whose strong balance sheets and reliable revenue streams are reassuring in a bank and credit crisis.

In America, First Republic Bank slumped nearly 90% while in Europe, beside Credit Suisse, Deutsche Bank were most in focus though they are now down by ‘just’ 20% after an earlier 30% fall. ING Groep and Société Générale by 15%-20% and, in the UK, Barclays and HSBC sank around 12% and Standard Chartered by rather more (their share price having been buoyed up in February by a mooted bid.

OPEC+ have thrown a spanner in the works with a surprise cut in output, clearly they have not been enjoying the steady decline in crude oil prices. How cheering to see this group demonstrating their selfless credentials in these inflationary times. This move has served to raise the price of oil though perhaps not as much as they might wish, it is up by a shade under 3% over this period.

Following a move wider in credit spreads over this period, we stick with our call to buy sterling corporate fixed interest (shorter-dated), it still looks like an attractive asset class. Equity markets are hard to call in general, but the UK equity does look like good value and I see a lot of cautious commentary and positioning out there...

The above article has been prepared for investment professionals. Any other readers should note this content does not constitute advice or a solicitation to buy, sell, or hold any investment. We strongly recommend speaking to an investment adviser before taking any action based on the information contained in this article.

Please also note the value of investments and the income you get from them may fall as well as rise, and there is no certainty that you will get back the amount of your original investment. You should also be aware that past performance may not be a reliable guide to future performance.

How would you like to share this?