In December last year we published an article Active managers and monkeys in the doghouse where we laid out the facts about how narrow global markets had got in 2025, with a rarefied handful of mega-cap Big Tech names having led the market for a remarkably long period of time, leaving the wider list of S&P constituents in their dust.

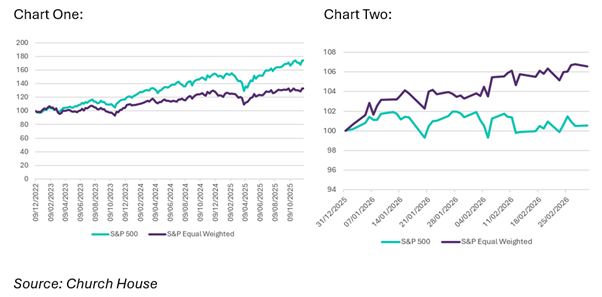

This can be seen most clearly on this three-year chart, showing the top-heavy S&P 500 vs the S&P 500 Equal Weighted Index (Chart One, right).

At the time we (oh so wisely) noted:

‘We currently see the widest positive diversion in performance of large caps relative to the wider market since dot.com – fuel for those calling an AI bubble in mega caps’

…and explored what could cause this to snap-back. With our hindsight glasses on, we were correct to be calling for a reversion to the mean but our reasons for this (less geopolitical uncertainty) and ongoing rate cuts were 50% correct at best.

The broadening of market leadership has been stark this year. To continue the above chart for 2026, one can see how quickly the market has moved (Chart Two, right).

The prevailing market psychology has changed from one of carpe diem to a nervy and skittish environment. While investors in 2025 were excited about the opportunity to profit from AI and keen to buy all potential “winners”, in 2026 the main worry is who the big casualties from this new technology will be? This has been seen most predominantly in the brutal sell-off in the shares of software companies globally, where business models are seen as ripe for attack from new AI-backed disruptors. It has been a market that sold first and asked questions later – just look at the negative move in stocks from Microsoft, to RELX, to London Stock Exchange Group. These are each fundamentally very different businesses, but if they are seen to be in the way of the AI train, investors have been ardent sellers.

The biggest winners of this flight from software have been more old world sectors such as Commodities, Industrials and even Consumer Staples – areas of the market that are seen as being less vulnerable to AI disruption. Investors are being uncharacteristically humble in admitting that they do not know the full ramifications of AI developments and so they are going back to basics by diversifying.

We have always stressed the benefits of suitably diversified portfolios as a core tenant of managing risk on behalf of our clients and feel that the broadening of markets in 2026 is a good thing that helps to take some of the equity risk off the shoulders of just a few enormous companies. That being said, we are also active managers and diversification for diversifications sake is not always positive or necessary. In the rubble of the software sector, for example, there will be some excellent businesses with moats sufficiently impenetrable to survive and even thrive in a world of AI developments. It is on us to roll-up our sleeves and carefully work our way through – a bit of old-fashioned stock picking.

The above article has been prepared for investment professionals. Any other readers should note this content does not constitute advice or a solicitation to buy, sell, or hold any investment. We strongly recommend speaking to an investment adviser before taking any action based on the information contained in this article.

Please also note that the value of investments and the income you get from them may fall as well as rise, and there is no certainty that you will get back the amount of your original investment. You should also be aware that past performance may not be a reliable guide to future performance.

How would you like to share this?